Make ZERO repayments for 8 weeks! Offer valid until April 30*.

Learn More

Key Takeaways:

Many SMEs struggle to secure the funding they need from banks, and COVID-19 has added another layer of complexity to the application process. But has the pandemic actually made it harder for SMEs to get a loan? How has it impacted lending?

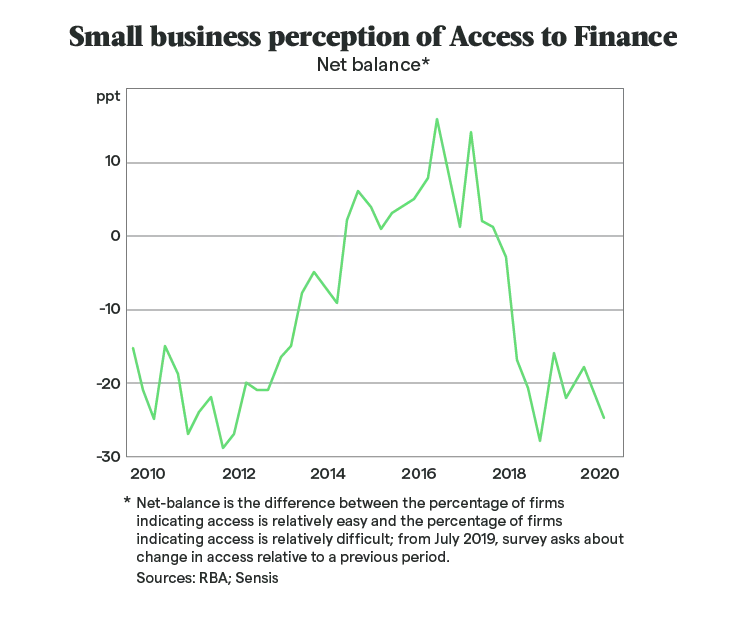

SME perceptions around accessing finance

Overall, small businesses believe that the pandemic has made it more difficult to qualify for a loan, let alone find affordable finance. For years this has been the case, but we’ve seen a steep decline in perceived accessibility for SMEs since the beginning of 2020:

The reality: has it actually become harder for SMEs to get a loan?

Banks have always lent to SMEs and startups more conservatively. Established organisations have been around longer, and as a result lenders can be more confident in their ability to meet repayment commitments.

SMEs are also twice as likely to default after taking out finance, compared to larger corporations and standard mortgage customers. And those who are approved are often left paying higher interest rates to compensate for the additional risk.

COVID-19 has only further tightened approval criteria for SMEs, and indeed it has become harder to get documentation over to lenders and eyes on applications.

While lending has tightened across the board, some industries are affected much more than others—in particular, those who have had to work around new COVID-19 restrictions or close shop completely. Lenders are less likely to offer funding to retail and tourism businesses as they've been hit the hardest by COVID-19. Other heavily affected industries include:

- Hospitality

- Education

- Airlines and businesses tied to airlines

- Hotels, motels and other accommodation services

- Bars, pubs and clubs

How have bankruptcy laws changed in response to COVID-19?

US-style insolvency laws have been recently developed to benefit SMEs currently facing insolvency.

Previously, businesses in this position would effectively lose control over their business, disincentivising them from entering the insolvency process until they absolutely had to.

The new laws will allow a small business operator to seek advice from an insolvency practitioner if they find themselves in financial distress.

Working together, the business operator and adviser will then have twenty days to create a plan outlining how they’ll restructure the business’ debt and prepare a case for creditors to assess.

Alternative finance from non-bank lenders

Cash flow issues have been a huge challenge for SMEs over the past six months, forcing them to think on their feet, adapt and make difficult decisions to stay afloat.

Non-bank lenders benefit SMEs with greater flexibility, leniency, speed, and a stronger focus on smaller business. Funding from alternative lenders (in cases where banks were not able to help) has therefore provided a lifeline for these businesses.

In a 2018 survey, findings concluded that non-traditional lending has increased in popularity since earlier in the decade.

If you're struggling to secure finance through a bank, chat to a Valiant lending expert about alternative options. We work with over 80 leading bank and non-bank lenders to connect businesses with the right finance solution for their needs.

Related articles

Here’s our latest selection of posts on running your business effectively with minimal fuss